Upgrade to Premium | Become A Sponsor

🙋 My Updates

Hi embedded finance friends,

Welcome to another edition of Embedded Finance Review. There are many updates from my end, as well as a fully packed newsletter. So let’s dive right in:

New design

As a regular reader, you will notice that the newsletter looks different than usual. I believe the new design makes it easier to read, but I would love your thoughts. As a next step, I will update my newsletter landing page, and I would like to add a couple of quotes from my readers. Please use the survey at the end of this newsletter to share your feedback about the new design and/or share a quote I could add to my new landing page.

Event sponsoring 2024

Last year, I hosted two Embedded Finance Review events in Hamburg and Berlin, and I am planning to have 2-3 events this year. Events have been slipping a bit on my to-do list, so I am currently re-focusing on event planning. For the first half of 2024, I am thinking of an event in Berlin (Mar/Apr) and another one in Amsterdam during Money2020 (early June).

Are you interested in sponsoring or partnering with an upcoming event? You can find Embedded Finance Review event details here, and if that sounds interesting, please get in touch with me (reply to this email).

Premium newsletter or sponsorship?

This is basically me thinking out loud here: I have plans to grow this newsletter and launch other activities in the embedded finance world (content, community, etc.). But all of this requires investment: money and time. Therefore, I thought about a) a premium subscription, which could include additional content, access to exclusive online events, and other community features; and b) including sponsors in the newsletter. Important: I have not made any decision, and this biweekly newsletter will remain free. But I am curious: how do you think about this? Would you be willing to pay for a premium subscription, and what needs to be included (if you want to show your support, you can already ‘upgrade’ today)? Would you still believe I am unbiased when I take sponsors on board? There are so many questions from my side; feel free to reply or use the survey at the end to share your thoughts.

But enough from me, this edition of Embedded Finance Review covers:

- 🛒 Retailer Sainsbury’s is following in Tesco's footsteps and announcing its decision to wind down its banking unit.

- 😖 Partner banks in the US are under pressure from the regulator

- ⬇️ Quote of the week: The less you see the embedded banking product, the better

- 📰 And many more news items, including Amazon shutting down their insurance store in the UK, a new card solution for the healthcare industry, and an embedded finance report about SaaS and marketplaces.

- 👨💻There are five jobs in the job board section

Sounds good? Let’s dive in 👇

🏢 Non-Financial Brands

British Retailer Sainsbury’s is winding down banking offering

Sainsbury’s Bank was originally launched in 1997 as part of a partnership between Sainsbury and Bank of Scotland, but Sainsbury’s took full ownership in 2014. The bank has already offloaded it’s mortgage book in the summer of last year and is now looking to exit the rest of its financial product offering, which includes loans, credit cards, and savings products. Sainsbury’s is likely to explore different options, including selling the bank to a competitor.

As a regular reader of this newsletter, this story will remind you of Tesco’s decision to sell Tesco Bank and, thus, exit financial services as well. Both retailers have had a similar approach to offering financial services and have now both decided that it does not make sense to continue this way.

A blow for embedded finance? Not really. Even though I have never used any of their products, it is probably fair to say that Sainsbury’s and Tesco Bank are much closer to a traditional banking offering than they are to an embedded finance product (perhaps except for the brand and having the stores as a customer acquisition channel). Most importantly, both companies have a banking licence of their own. When you read the official announcement from Sainsbury’s, you will understand that offering financial services is still very attractive for them; however, the model (=own licence) is not suitable anymore, most likely due to high costs and regulatory burden. Sainsbury’s even emphasises that it is looking at a distribution model of financial products, similar to its insurance product offering.

The financial world and customer demands have changed a lot since these retailer banks were founded, so a fundamental change to the model seems overdue. I believe it is the right decision to move away from an own licence and partner with one or more financial institutions (note: neither approach makes it immediately ‘embedded finance’ and other things need to be in place). However, I also believe that retailers have a tough nut to crack when it comes to embedded finance. But that is probably worth it’s own post in a future edition.

🇬🇧 Amazon shuts down it’s insurance store in the UK. I have read a few LinkedIn posts about the announcement, and most of them mentioned various strategic mistakes (i.e., not hiring industry experts or focusing on the wrong parts of the value chain).

🇬🇧 Lettspay, a UK landlord software solution that includes bank accounts, shares details on this podcast with its banking partner Griffin.

🇳🇱 Booking.com and Mastercard have joined forces to simplify B2B travel payments and improve the overall travel experience.

🇸🇪 Spotify to launch in-app shopping in EU, Enabled by the DMA Rollout.

🇮🇪 Airline Aer Lingus partners with Revolut and integrates the new Revolut Pay product (Link). The solution aims to reduce friction by cutting down on the number of steps as well as decreasing the possibility of fraud.

🇺🇸 Airbnb raises guest service fees by 2% for cross-currency bookings and says “we adjust our fees to align with the value we provide our guests.”

🇮🇳 Healthcare and insurance providers in India can leverage a new platform for claims powered by Mastercard. The end-to-end solution works by seamlessly embedding virtual cards within the health tech platforms.

🏗️ Infrastructure Provider

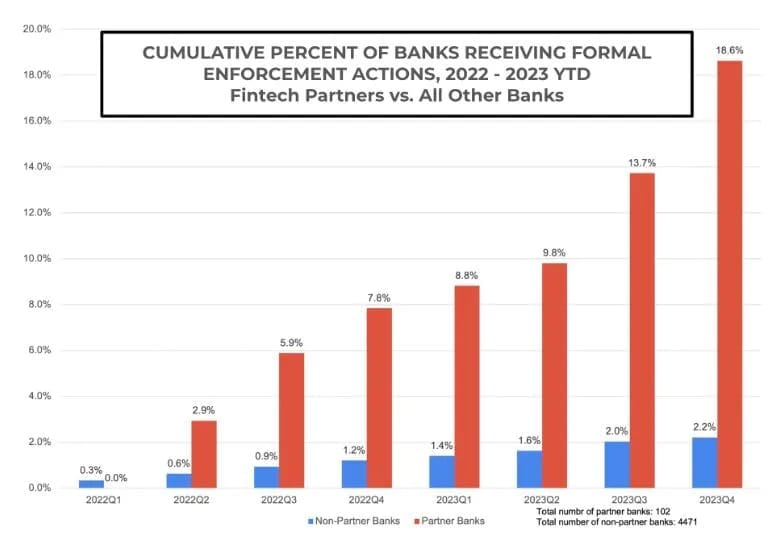

US Sponsor banks are under pressure

When a company (fintech or brand) wants to launch a financial product in the US, there are basically no alternatives other than to partner with a traditional bank. This is due to the fact that there are no licences like the e-money licence that we have in Europe and because it’s really hard to apply for a bank licence on your own. Those banks that work with a fintech or brand to offer financial products are called ‘partner banks’ (or sponsor banks).

Now take a look at the graphic above again (Source) and you will understand that a bank that partners with a fintech company or a brand is a lot more likely to receive formal enforcement actions compared to a bank without such partnerships. As mentioned before, an embedded finance or even fintech product in this matter requires many different partners, and it relies on the fact that every party is doing what they are supposed to do. In an ideal world, this works smoothly, but reality can be different.

And there is one bank that is getting a lot of attention from the US regulator: Blue Ridge Bank, which just received its second enforcement action from the federal regulator, the OCC. The bank is known for its fintech partnerships, including its partnership with Unit, an embedded banking provider in the US. The link above mentions the different points the regulator addresses, but at the end, most of them fall into the category of failures in overseeing and enforcing compliance requirements (i.e., how does my fintech partner onboard its customers, how do they angle certain processes around processes, and so on). The model of embedded finance requires a well-working partnership of frontend, technology, and compliance (or non-financial brands, infrastructure providers, and licence holders). Many banks have become sponsor banks in the last few years, and they might have underestimated the complexity and effort required. But they need to catch up because fintech companies and non-financial brands are now more likely than ever to take compliance into their decision making matrix when choosing a partner bank.

🇬🇧 The embedded insurance provider Qover announces the launch of its motor insurance solution in the UK, which enables car manufacturers to provide digital insurance programmes across Europe.

🇬🇧 Embedded lending provider YouLend announces the completion of a debt partnership with J.P. Morgan and Castlelake. The deal will enable YouLend to extend £4 billion in additional revenue-based financing to small and medium-sized enterprises (SMEs).

🇩🇪 B2B buy now, pay later startup Mondu is set to expand across Europe after securing €30 million in debt financing from Vereinigte Volksbank Raiffeisenbank.

🇺🇸US-based embedded banking Alviere has announced a partnership with Onafriq, an Africa-based payments network. Alviere operates in the US and had previously ambitions to expand to the UK and EU, but has shut down these expansion efforts.

🇺🇸 Cybrid adds B2B payment capabilities to its embedded finance API solutions.

🇦🇷 Latin American payments startup Pomelo raises $40 million led by VC Kaszek. Pomelo says it will use the new funding to double the size of its business over the next year.

🇧🇷 Visa closes Pismo acquisition, which was announced in June 2023.

🤓 Knowledge section

❝ “the less you see the embedded banking product, the better” Paul Staples (ClearBank)

Quote of the week

In the last newsletter, I shared ClearBank’s announcement to enter embedded finance and the hiring of industry veteran Paul Staples. I caught up with Paul after that, and we chatted about various embedded finance topics. During this chat, he dropped the sentence above where he spoke about one of his previous embedded finance projects. What did he mean? When different teams are responsible for different parts of the product, you might end up in a situation where each team tries to increase their visibility. Obviously, that is wrong, and nothing else but customer value and experience should be focused on. Instead, Paul suggested, a product team responsible for an embedded finance product should aim for less, not more surface area.

Do you agree? Would you like to see a regular “quote of the week” section in this newsletter? I guess you know by now how to let me know: survey at the end of this newsletter 🙃

📈 Aperture and Swan teamed up and created a report highlighting Embedded Finance in SaaS platforms and marketplaces.

📕 FT Partners publishes its fintech outlook for 2024: The fintech journey continues (page 29 for embedded finance).

🧑⚖️ EU shares a new rulebook to fight money laundering and German regulator BaFin increases focus on IT outsourcing risks.

🤓 Kelvin Tan, the CEO of Audax, a BaaS corporate venture from Standard Chartered, shares insight into their journey and approach to BaaS.

🎿 Facing the Future: Banks are at the Crossroads of Embedded Finance.

🇮🇳 India partners with Google Pay to take its payment infrastructure UPI global.

👨💻 Job Board

1️⃣ Head of Product at an expense management solution (new)

2️⃣ Head of Payments at an automobile-focused payment provider

3️⃣ Business Development Manager at an automobile-focused payment provider

4️⃣ VP Marketing at an embedded banking provider

5️⃣ CFO at an embedded lending provider

Does one of these roles sound interesting to you? Hit reply, and I will tell you more!

Are you hiring? Send me the details and get featured in the next edition.

🔄 Your support

Somebody forwarded you this email? Subscribe for free.

Are you planning to start your own newsletter? Check out Beehiiv.